A Report On The Energy Market

Bills are driven by both the price of energy on the wholesale market and Third Party Costs (TPCs). TPCs include non-energy costs set by the government, network, policy and system costs and electricity transmission/distribution costs. The biggest single cost on a bill is the price of the energy. The wholesale cost of the energy makes up approximately 45% of an electricity bill and 65% of a gas bill, with the remaining being TPCs, which have been continuously rising in recent years, and can be volatile.

This pricing report focuses on the energy element of a bill to help you keep track and understand the wholesale energy market and the factors affecting the price of your contracts.

Gas and Power

Weaker trading within the UK carbon and gas markets combined with up to 16 LNG (Liquefied Natural Gas) vessels expected into the UK in the coming weeks has resulted in the prices of electricity and Gas contracts to decrease further each day this week.

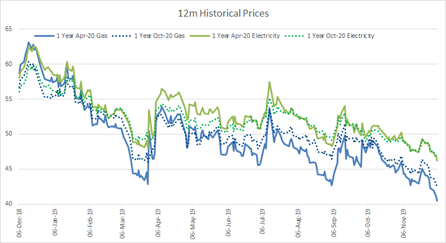

Electricity contract prices peaked in August 2018, almost reaching £70/MWh but are currently at just above £40/MWh which is the lowest they have been since August

NOW IS AN OPPORTUNE TIME TO LOCK IN A PRICE AS INCREASED WIND GENERATION AND A BEARISH SUPPLY OUTLOOK PUT PRESSURE ON CONTRACTS, KEEPING PRICES LOW.

Crude

Brent initially weakened early in December following President Trump’s appearance of being happy with playing the long game against China.

The losses were then reversed, and Brent increased in price as attention returned to the OPEC meeting ending with the market expecting deeper production cuts. (Currently, there is an oversupply of oil. If deeper cuts are made by OPEC it will result in the global supply of oil to decrease, which will increase the demand and therefore price).

Shortly after, Brent crude reversed some of the previous session gains but is still trading 7.4% higher than the start of October.

Oil

The API report issued week commencing 2nd December 2019 showed that Crude US inventories fell by more than anticipated against the previous week. According to the API, there were 3.7 million barrels drawn against the prediction of 1.5-1.7 million, which reversed the downward trend and sent the trade price of Brent upwards.

Supporting the increase in prices are OPEC and the OPEC+, meeting in the same week as they faced the fact that global oil supply could continue to rise at a rapid pace in 2020, surpassing the increase in demand. It has been reported that they considered cutting production by an additional 500,000 barrels per day as their biannual meeting kicked off in Vienna.

The Russian Energy Minister has revealed they will adhere with current agreed levels of production, whilst a competitor to the state-owned producer allegedly said that further curbs in winter would not be wise. However, Saudi Arabia would love a higher oil price in the lead up to Saudi Aramco IPO and have reportedly been lobbying other producers of increasing cuts

The surge in output complicates OPEC’s task as the meeting approaches. If the predictions are correct and global supply growth is expected to surge this year, the group risks a price crash if it doesn’t make further cutbacks on production levels.

US-China

Prices fell slightly due to President Trump indicating that he was in no rush to finalise a trade deal with China and happy to wait until the next election which takes place in November this year.

However, as the global economies continue to slow down, American tariffs are set to rise which could have a knock-on effect on the trade price of oil and therefore contract prices in coming weeks.

So if you feel it’s about time you reviewed your costs, we can help you compare some of the best tariffs available right now to set you up for the year.